Tokenization

Series: Own Your Tokens — Part 3 of 3

The first two articles in this series established the foundational architecture: why PAN custody determines strategic independence, how vault ownership is the first decision that either locks you in or sets you free, and how the Network Token market has developed a structural pattern of delivering genuine token benefits through architectures that merchants don't own.

This final article covers three remaining areas — Device Tokens from mobile wallet flows, Merchant Tokens as the merchant-sovereign layer that makes everything else composable, and Token Lifecycle Management as the operational discipline that determines whether your token infrastructure actually performs over time.

It closes with a five-point audit framework for assessing any existing stack against the credential sovereignty criteria this series has established.

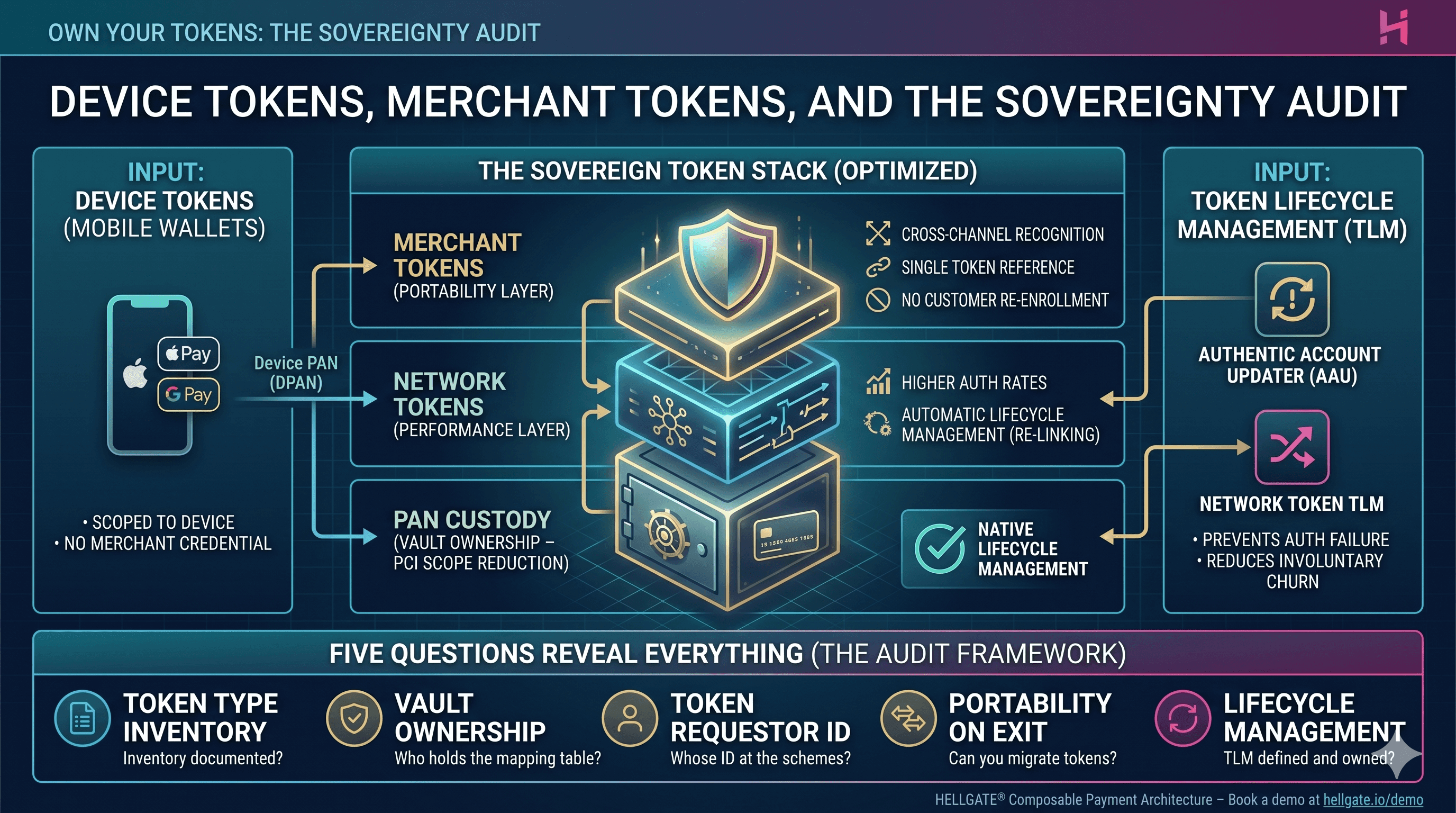

Device Tokens: When the PAN Never Leaves the Device

Mobile wallet payments — Apple Pay, Google Pay, Samsung Pay — operate on a fundamentally different tokenization model than anything discussed so far. Understanding how Device Tokens work, and what they mean for merchant infrastructure, is increasingly important as mobile wallet volume scales.

The technical architecture

When a cardholder provisions a payment card into Apple Pay or Google Pay, the card network issues a Device PAN (DPAN) — a token specific to that device's provisioning event. The DPAN is stored in the device's Secure Element or equivalent trusted execution environment. The Funding PAN (FPAN) — the actual card number — never leaves the issuer and the network.

At transaction time, the merchant terminal or payment SDK receives the DPAN alongside a dynamic cryptogram generated uniquely for that transaction. The cryptogram is bound to the specific transaction context — amount, merchant, timestamp — making it non-replayable. The FPAN never appears in the transaction flow.

This is not a marketing abstraction. It is the actual token architecture, and its security properties are genuine: the merchant never processes the cardholder's real card number in a mobile wallet transaction.

Operational implications for merchants

Device scoping. A DPAN is valid only on the device where it was provisioned. A cardholder who replaces their handset triggers a new provisioning event, generating a new DPAN. This is handled automatically by the wallet provider — but it affects cross-device analytics and stored credential logic. If your system attempts to correlate payment events across devices using token values, Device Token scoping will produce fragmented cardholder views.

No direct merchant credential. Device Tokens are not a stored credential type that merchants can hold and re-use for recurring billing. They are single-use in the sense that each transaction generates a fresh cryptogram. The DPAN value remains constant across transactions on the same device, but it is not a portable credential that the merchant can route through a different acquirer or reference independently of the wallet infrastructure.

Interaction with PCI token layer. As mobile wallet volume scales, the architectural question is how DPANs interact with your existing PCI vault and Network Token infrastructure. A DPAN received in a transaction needs to be handled consistently with your token governance model — whether that means vault storage for analytics, mapping to a merchant-side reference token, or pass-through processing. The interaction between these layers needs deliberate design, not default behavior.

Where Device Tokens sit in the sovereignty picture

Device Tokens don't resolve the credential sovereignty question. The PAN remains with the issuer and the network — not with the merchant, but also not with any gateway. For transaction flows where the customer is present and using their wallet, this is an acceptable outcome: no party in the merchant's stack holds the PAN.

For stored credential use cases — subscription billing, card-on-file, one-click checkout — Device Tokens are not the right mechanism. Those flows require either a PCI-vaulted PAN under merchant control, or a Network Token issued against that PAN and managed through the merchant's Token Requestor infrastructure.

Merchant Tokens: The Portability Layer

Of all the token types discussed in this series, Merchant Tokens are the least marketed and the most strategically important.

A Merchant Token is a surrogate value issued by the merchant — or by an infrastructure provider operating exclusively under the merchant's control — with the token-to-PAN mapping table residing in merchant-controlled infrastructure. Not at the PSP. Not at the network. With the merchant.

This single fact changes the operational calculus for every downstream provider relationship.

What Merchant Tokens make possible

PSP-independent recurring billing. A Merchant Token linked to a stored PAN remains valid regardless of which acquirer processes the next transaction. When you change PSPs, the token doesn't change — you re-route the authorization request through a new downstream provider while referencing the same stored credential. Zero customer re-enrollment. The transition is invisible to the cardholder.

Omnichannel credential consistency. A cardholder paying online, in-app, and at POS can be recognized through a single Merchant Token — because the merchant controls the mapping across all channels. Gateway-issued tokens fragment this: each channel typically operates within its own token domain, owned by the respective provider. The merchant ends up with multiple token representations of the same underlying card, held in multiple provider systems, with no coherent cross-channel view.

Multi-acquirer routing and optimization. With merchant-controlled token infrastructure, authorization routing logic lives in the merchant's orchestration layer. Volume can be split across acquirers, fallback to a backup acquirer on decline, or A/B tested for authorization rate performance — without renegotiating token portability with any single provider. The token stays constant; the routing changes.

Resilience against provider failures. If your primary PSP experiences downtime, merchant-controlled tokens allow immediate failover to a secondary acquirer without any credential re-collection. The token inventory is independent of any single provider's operational status.

Merchant Tokens in the token stack

Merchant Tokens are not a replacement for PCI vault tokens, Network Tokens, or Scheme Tokens. They operate as a different layer — the merchant-side reference layer that maps to underlying network credentials and enables portable orchestration.

In a well-designed token architecture, the layers interact as follows:

The PAN lives in a merchant-controlled vault, isolated for PCI scope reduction

Network Tokens are issued against the PAN through a Token Requestor operating under the merchant's identity — carrying the auth rate benefits and lifecycle management of network-level credentials

Merchant Tokens provide the merchant-side reference that persists across provider relationships, enabling routing logic and omnichannel consistency without exposure to the underlying credential

Without Merchant Tokens — or merchant-controlled vault infrastructure — the composability of this architecture collapses. The merchant ends up dependent on each provider's token domain, unable to route freely or migrate without customer-facing disruption.

Token Lifecycle Management: The Silent Auth Rate Problem

Tokens degrade over time if lifecycle management is absent or inadequate. Cards expire. Cardholders receive replacements. Issuers block cards for fraud. Each of these events can invalidate a stored token — and in subscription and card-on-file models, invalidated tokens translate directly into failed authorizations and involuntary churn.

This is one of the highest-ROI problems in payment operations, and one of the least visible in standard reporting.

The two lifecycle mechanisms

Automatic Account Updater (AAU). Visa and Mastercard operate account update services that push new card data to enrolled merchants when a card is renewed or replaced. When enrollment is active and the update is processed correctly, stored credentials stay current without any action from the merchant or customer. The prerequisite is enrollment: the merchant, or their Token Requestor, must be registered with the relevant network for each card scheme.

Network Token Lifecycle Management. For transactions using genuine Network Tokens, the network manages lifecycle at the token layer directly. When an issuer marks a card as renewed, blocked, or replaced, the network can update the token mapping — re-linking it to the new account details — without any merchant action, without AAU polling, and without customer re-entry. This is one of the most operationally significant advantages of Network Tokens over PAN-based stored credentials: lifecycle is handled at the infrastructure layer, not the application layer.

What happens when neither is in place

Stored tokens go stale. The first indication is typically a decline rate increase on recurring charges — often subtle enough to be attributed to issuer behavior rather than credential quality.

Over time, the pattern compounds: failed charges trigger dunning flows, customers who complete re-enrollment represent a recoverable fraction, and customers who don't represent permanent involuntary churn. For subscription businesses, the cumulative impact of poorly managed token lifecycle is measurable in cohort retention curves — but it rarely appears as a line item in payment operations reporting.

Authorization rate improvements of 2-5 percentage points are achievable through lifecycle management alone, in stacks where it has previously been absent or inadequate. That is among the highest-return payment infrastructure investments available.

The question to ask

For any tokenization infrastructure in your stack: who manages token lifecycle — the merchant, the PSP, the network, or nobody?

If the answer is nobody — or if the answer is unclear — you have a measurable revenue leak that has a known solution.

The Sovereignty Audit: Five Questions for Any Payment Stack

The preceding articles and this one have established a framework for evaluating credential sovereignty across any payment stack. Here it is in a form suitable for direct use in vendor evaluations, infrastructure reviews, or internal payment architecture assessments.

Question 1: Token type inventory

What token types are actually in production in your stack?

PCI vault tokens, Network Tokens, Gateway Tokens, Device Tokens, Merchant Tokens — or an undocumented combination? Many merchant stacks contain multiple token types across different channels, often without a coherent map of which type is used where, who issued each, and under what ownership model.

If this inventory doesn't exist, it's the necessary starting point for any sovereign token architecture.

Question 2: Vault ownership

Who operates the token vault? Who holds the token-to-PAN mapping table?

Is the vault operated by your PSP, a dedicated third-party infrastructure provider, or your own infrastructure? What are the contractual terms around data portability on contract termination? Is token export technically supported — and has it ever been tested?

If the vault is PSP-operated and token export has never been exercised, the practical switching cost is significantly higher than the contractual switching cost.

Question 3: Token Requestor ID

For every Network Token in your stack: under whose Token Requestor ID is it registered with Visa or Mastercard?

If the answer is your provider's Token Requestor ID, those tokens cannot be ported. The switching cost is calculable: it is proportional to the number of stored credentials in that token domain. Each one represents a customer who would need to re-enroll on provider migration.

If the answer is your own Token Requestor ID, or a setup where an independent provider manages tokens under a merchant-controlled identity, the tokens are portable and the architecture is sovereign.

Question 4: Portability on exit

If you terminated your current PSP relationship with 30 days notice: which tokens could you migrate, which would require customer re-enrollment, and what is the operational impact on subscription billing, card-on-file flows, and one-click checkout?

This question is best answered before signing a contract, not after receiving a termination notice. Providers with genuinely portable token infrastructure can give specific, technical answers. Providers without it tend to answer in generalities.

Question 5: Lifecycle management ownership

Who manages token updates when cards expire or are re-issued?

Is Automatic Account Updater active and enrolled for all relevant card schemes? Are Network Token lifecycle events handled at network level — or does your stack rely on merchant-triggered polling, manual re-collection flows, or customer-facing dunning?

If lifecycle management is undefined or delegated without explicit SLA to a provider, the authorization rate impact is measurable and the fix is known.

Conclusion: Tokenization Is an Ownership Decision

Payment tokenization is frequently presented as a compliance project — a mechanism for reducing PCI scope and securing card data. It is that. But it is also something more consequential: the architectural layer that determines whether your payment stack is an asset you control or a service you rent on someone else's terms.

The token types, the vault ownership model, the Token Requestor ID structure, the lifecycle management approach — these are not technical footnotes. They are the decisions that determine your ability to switch providers, optimize authorization rates competitively, run omnichannel payment flows coherently, and build payment infrastructure that compounds in value over time rather than embedding switching costs that grow with every stored credential.

Owning your tokens means owning the mapping table. It means knowing whose Token Requestor ID your Network Tokens are registered under. It means operating vault infrastructure that serves your interests, not your provider's. It means lifecycle management that keeps your stored credentials current without depending on any single party's operational discipline.

Own your tokens. Own your stack.

Own Your Tokens is a Hellgate® editorial series on payment tokenization, credential sovereignty, and the architectural decisions that determine who controls your payment stack.

Hellgate® offers Guardian — a merchant-controlled PCI vault and tokenization component — as part of the Composable Payment Architecture. Book a demo at hellgate.io/demo or explore the documentation at developer.hellgate.io.

Jens Kohnen was driven to co-start the company by the conviction that payment infrastructure should empower businesses, not bind them. Recognizing that many large organizations were locked into monolithic, opaque setups, Jens embarked on a journey to free enterprises from these rigid stacks. His mission is to enable companies to regain full ownership and monetize their flows, transforming payments from a cost center into a strategic lever for growth.