T

C

Card Acquiring

Card Acquiring is the process by which banks or financial institutions accept credit and debit card payments on behalf of merchants, managing settlement and risk.

Card Acquiring Definition

Card Acquiring is the technical and financial process enabling merchants to accept payment transactions from cardholders using credit, debit, or prepaid cards.

It involves an Acquiring Bank (or Acquirer) that contracts with the merchant to maintain a merchant account, authorize transactions via card networks (Visa, Mastercard, etc.), and settle funds.

Ideally, the acquirer assumes the risk of merchant solvency and ensures funds are transferred from the Issuing Bank to the merchant’s account.

Deep Dive: The Mechanics of Acquiring

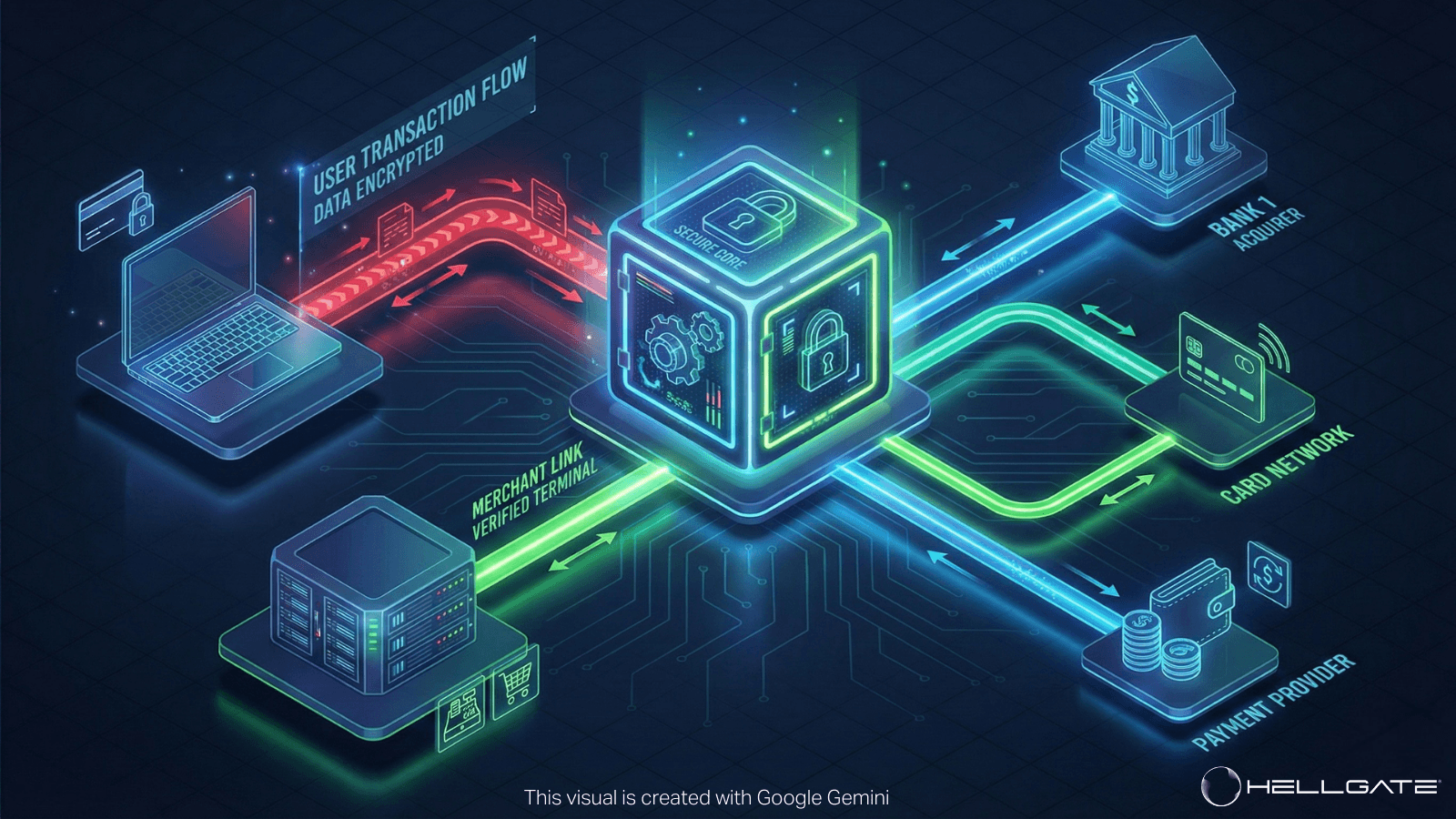

Card acquiring is not a single event but a synchronized workflow involving data transmission, risk assessment, and liquidity movement.

The process is generally bifurcated into the Front-End (Authorization) and Back-End (Clearing and Settlement).

1. Authorization (The Technical Handshake)

When a consumer taps or inserts a card, the transaction data travels through a complex chain in milliseconds.

Capture: The Point of Sale (POS) or Gateway captures the card data (PAN, expiry, CVV) and cryptograms.

Routing: The Acquirer (or their processor) formats this data into an ISO 8583 message and routes it to the appropriate Card Scheme (e.g., VisaNet).

Decisioning: The Scheme forwards the request to the Issuing Bank. The Issuer checks funds/credit limits and fraud scores, returning a response code (e.g., 00 for Approval).

Response: The Acquirer relays this response back to the merchant to finalize the sale.

2. Clearing and Settlement (The Financial Movement)

Authorization only guarantees that funds exist; it does not move money.

Batching: At the end of the trading day, the merchant submits a batch of authorized transactions to the Acquirer.

Clearing: The Acquirer sends these batch files to the Card Schemes, which calculate the net amounts due between Issuers and Acquirers.

Settlement: The Card Schemes debit the Issuers and credit the Acquirers. The Acquirer then funds the merchant, usually minus the Merchant Discount Rate (MDR) and Interchange fees.

Strategic Importance in Modern Payments

For high-volume merchants, Card Acquiring is no longer a commodity; it is a strategic lever for revenue optimization.

Acceptance Rates: Not all acquirers perform equally across all geographies. An acquirer with local licenses in a specific region (e.g., Brazil or Japan) will typically achieve higher authorization rates for local cards than a cross-border acquirer due to lower fraud flags from Issuers.

Cost Structure (Interchange++ vs. Blended): Sophisticated merchants prefer acquirers offering Interchange++ pricing, which provides transparency into the specific interchange fees, scheme fees, and acquirer markup, rather than opaque "blended" rates.

Data Richness: Modern acquirers provide Level 2 and Level 3 data transmission (passing line-item detail like tax ID and freight amount), which effectively lowers interchange rates for B2B and corporate card transactions.

Acquiring vs. Processing vs. Gateway

Confusion often arises between these terms as many providers bundle them. Payment Gateway: The technical "pipe" connecting the checkout to the processor. It encrypts data but does not touch the money. Payment Processor: The technical engine executing the transaction. They connect to the card networks. Acquirer: The financial institution (member of the card scheme) holding the license and underwriting the merchant risk. Note: Many modern fintechs act as "Full-Stack" providers, combining gateway, processing, and acquiring functions.

Common Pain Points in Traditional Acquiring

Merchants relying on a single acquiring partner often face operational bottlenecks that stifle growth.

Vendor Lock-in: Relying on one acquirer creates a single point of failure. If the acquirer experiences downtime or freezes funds due to a risk flag, the merchant’s revenue stream halts immediately.

Cross-Border Inefficiencies: Using a domestic acquirer for international transactions results in high FX fees and low approval rates, as foreign issuers often decline transactions originating from unfamiliar acquiring banks. Opaque

Pricing: Traditional statements often obscure the breakdown of fees, making it impossible to audit Interchange costs or negotiate better markups.

The Hellgate Approach:

Composable Acquiring Strategy

In a modern payment stack, a "one-size-fits-all" acquirer is obsolete.

Enterprise merchants require a Composable Payments Architecture (CPA) to decouple the acquiring layer from the technical integration.

Hellgate® CPA enables this by treating Card Acquiring as a modular component rather than a hard-coded dependency.

Agnostic Connectivity: Through the Link module, merchants can connect to multiple acquirers globally via a single API. This allows a merchant to use a local acquirer in the EU for SEPA compliance while using a different, high-risk specialized acquirer for specific vertical transactions in the US.

Redundancy and Optimization: By utilizing multiple acquirers, the Hub (Orchestration) module can dynamically route transactions. If the primary acquirer is down or declines a transaction, Hellgate automatically fails over to a secondary acquirer to recover the revenue.

Unified Reconciliation: Regardless of how many acquirers are in the stack, CPA normalizes the settlement data, providing a single source of truth for finance teams.

FAQ

Q: What is the difference between an Issuer and an Acquirer?

A: An Issuer (Issuing Bank) provides the card to the consumer and pays for purchases. An Acquirer (Acquiring Bank) processes the payment for the merchant and receives the funds.

Q: Why do merchants need multiple acquirers?

A: "Multi-acquiring" increases resilience and optimizes costs. It prevents total outages if one provider fails and allows merchants to route transactions to the acquirer offering the lowest fees or highest approval rates for a specific region.

Q: What is a Merchant Identification Number (MID)?

A: A MID is a unique code provided by the Acquirer to identify a specific merchant account during the transaction processing flow.

Q: Does the Acquirer handle fraud detection?

A: Basic checks (AVS, CVV) are handled during authorization. However, sophisticated fraud prevention usually requires a dedicated risk engine like Hellgate Specter to analyze behavioral biometrics before the transaction reaches the acquirer.