T

E

Embedded

Embedded Finance

What is Embedded Finance?

Embedded Finance refers to the seamless integration of financial services-such as payments, lending, insurance, or debit card issuance-into the user interfaces of non-financial platforms. Instead of redirecting a user to a third-party banking portal, the platform (e.g., a ride-share app, SaaS ERP, or e-commerce marketplace) consumes financial APIs to offer these services natively. This creates a unified experience where the financial transaction is an invisible, functional layer of the core product, rather than a standalone event.

Deep Dive: The Architecture of Invisible Banking

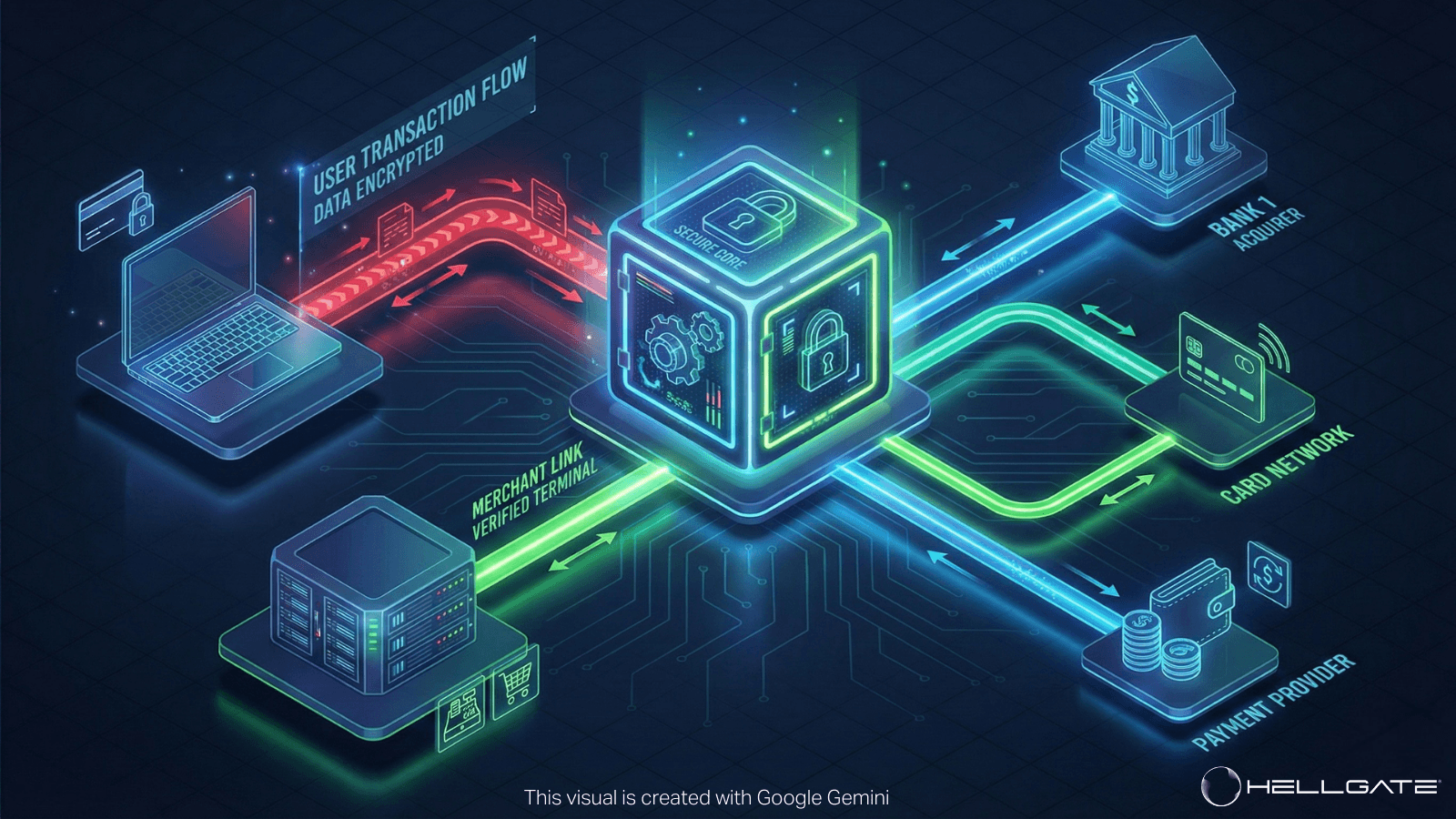

Embedded Finance represents the shift from "Banking as a Place" to "Banking as a Service (BaaS)." It requires a highly modular technology stack to function.

1. Technical Mechanics: The API Layer

The architecture typically involves three stakeholders: the Brand (Frontend), the Enabler (Middleware/Orchestrator), and the License Holder (Bank).

The Brand (Frontend): The non-financial platform (e.g., a gig-economy app) builds the user interface. They use SDKs to collect KYC data and initiate transactions.

The Enabler (Middleware): This layer abstracts the complexity of the banking rails. It exposes RESTful APIs for creating accounts, issuing virtual cards, or triggering ACH transfers. It handles the translation between modern JSON payloads and legacy banking file formats (NACHA, ISO 20022).

The Ledger: A core component of embedded finance is the "Shadow Ledger." The platform must track balances, pending authorizations, and settlements for thousands of sub-merchants or users in real-time, independent of the bank's daily batch processing.

2. Strategic Importance

Monetization (The "Vertical SaaS" Thesis): By embedding payments, software platforms can increase revenue per user (ARPU) by 2–5x. Instead of just charging a subscription fee, they earn a take rate (basis points) on every dollar flowing through their system.

Stickiness & Retention: When a business uses a platform not just for workflow (e.g., booking appointments) but also for financial management (e.g., receiving payouts, spending via issued cards), switching costs become prohibitively high.

Contextual Data: Platforms possess contextual data that banks lack. A logistics platform knows exactly when a driver completed a route, allowing them to offer instant credit or insurance based on real-time activity rather than generic credit scores.

3. Comparison: Traditional vs. Embedded

Feature | Traditional Fintech Model | Embedded Finance Model |

User Journey | Redirect to PayPal/Bank Portal. | Native, in-app experience. |

Brand Control | Low (Bank's brand visible). | High (White-labeled). |

Revenue | Referral fees (small). | Interchange/Processing fees (high). |

Data Access | Siloed at the bank. | Shared with the platform. |

Onboarding | Days (Manual KYC). | Minutes (Automated eKYC). |

Common Pain Points in Implementation

For platforms attempting to build this stack from scratch, the barriers are significant:

Regulatory Burden: Becoming a registered Payment Facilitator (PayFac) or securing banking licenses takes years and millions in legal fees.

Ledger Integrity: Building a double-entry accounting system that can handle split payments, refunds, and multi-currency settlements without errors is a massive engineering undertaking.

Compliance Ops: You must build operational teams to handle OFAC screening, AML (Anti-Money Laundering) alerts, and KYC document manual reviews.

The Hellgate Approach

Hellgate provides the "Enabler" infrastructure, allowing platforms to launch embedded financial products without becoming a bank.

Link (Connectivity): Acts as the unified gateway. Whether you are embedding payments into a mobile app or an In-Car Payment system, Link provides the single API connection to global banking rails, abstracting the fragmentation of underlying acquirers.

Commerce (Lifecycle Engine): The operational backbone. Hellgate Commerce includes a pre-built ledgering system that handles the complex "money movement" logic-automating payouts to sub-merchants, calculating platform fees, and managing refunds-so your engineering team doesn't have to build a core banking system.

Guardian (Compliance): To reduce regulatory scope, Guardian handles the capture and tokenization of sensitive KYC/KYB data, ensuring that while you own the customer relationship, you do not hold the toxic liability of raw PII.

Frequently Asked Questions (FAQ)

Q: Do I need a banking license to offer Embedded Finance?

A: No. Most platforms operate as "Program Managers" or "Agents" of a chartered bank partner. Middleware providers (like Hellgate) often facilitate these relationships or operate under an FBO (For Benefit Of) structure.

Q: What is the difference between Embedded Payments and Embedded Banking?

A: Embedded Payments refers to accepting money (checkout). Embedded Banking refers to storing and moving money (issuing cards, holding balances, lending).

Q: Can I implement Embedded Finance for B2B?

A: Yes. B2B platforms are the fastest-growing sector. Use cases include automated invoice factoring, issuing virtual corporate cards for employee expenses, and real-time vendor payouts.

Q: How does this impact my PCI scope?

A: If done correctly using components like Hellgate Link, your scope remains low (SAQ-A). You use secure fields to capture data, meaning the raw financial details never touch your backend servers.